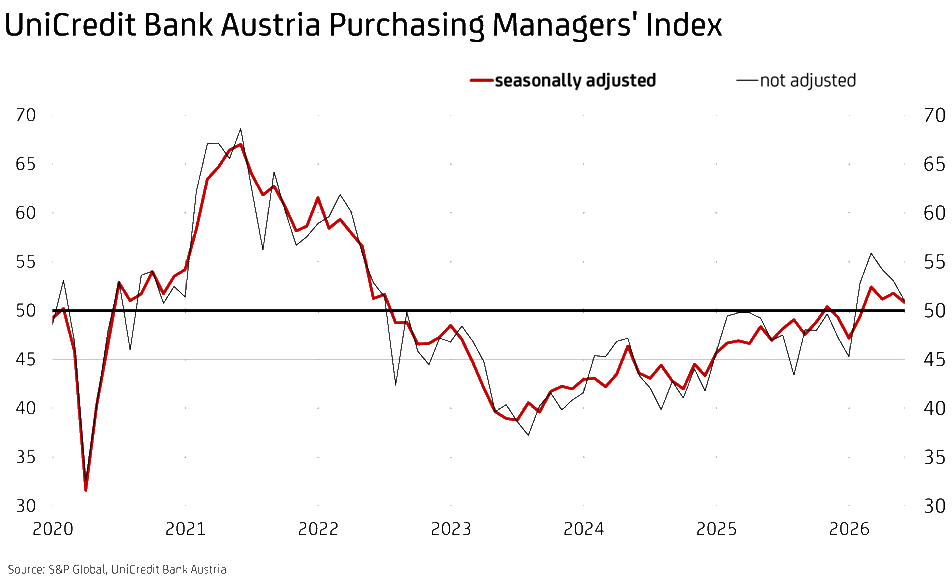

UniCredit Bank Austria Purchasing Managers’ Index in June

Inventory build-up keeps Austria’s industry on a growth trajectory

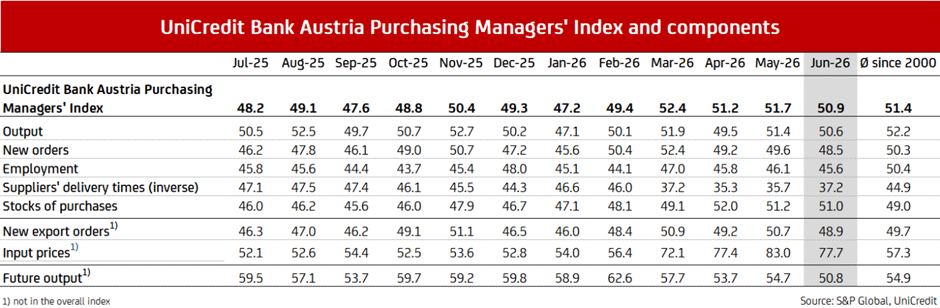

- The UniCredit Bank Austria Purchasing Managers’ Index fell to 50.9 points in June

- Geopolitical uncertainties dampened optimism: business expectations over the coming year fell to 50.8 points in June, the lowest level in one and a half years

- Despite the accelerated decline in new business, companies expanded production slightly

- Employment in the domestic manufacturing sector has been falling for three years, and in June the rate of decline accelerated compared with the previous month

- Reduced supply concerns and fewer worries about price distortions led to a further slowdown in the build-up of stock

- Lower energy prices eased pressure on purchase and selling prices

Austrian industry continued its moderate growth trajectory at the end of the second quarter. “At 50.9 points in June, the UniCredit Bank Austria Purchasing Managers’ Index was once again above the 50-point threshold, which signals growth. However, the 0.8-point decline compared with the previous month points to a slowdown in momentum”, says UniCredit Bank Austria’s Chief Economist Stefan Bruckbauer, adding: “Companies’ assessment of future business developments has also deteriorated significantly at the mid-year point. The index for expectations regarding business performance over the coming twelve months fell to 50.8 points. This is the lowest figure in one and a half years and is well below the long-term average. However, most of the feedback included in the calculation was received before the signing of the framework agreement to cease hostilities between the US and Iran. An easing of the geopolitical situation and the resulting gradual normalisation of economic conditions should quickly restore optimism among domestic businesses.”

Following a 3 per cent rise in production last year, manufacturing output achieved year-on-year growth of 0.8 per cent in the first quarter, despite the outbreak of the war in Iran. The average reading of the UniCredit Bank Austria Purchasing Managers’ Index of 51.3 points in the second quarter signals sustained growth in the sector despite the difficult operating conditions.

“Given that the war in Iran is expected to come to a definitive end, the geopolitical situation – and with it the supply chain issues and commodity price situation linked to the blockade of the Strait of Hormuz – should gradually ease in the second half of the year. Industrial activity is likely to benefit from this, and the recovery trend – which has been very moderate so far – is expected to gain momentum in the coming months. We expect real industrial production in Austria to rise by 1.5 per cent for 2026 as a whole”, said Bruckbauer.

The current 0.8-point month-on-month decline in the UniCredit Bank Austria Purchasing Managers’ Index was attributable to a deterioration across all components. “Domestic firms increased their production in June at a slower pace than in the previous month, primarily as a result of a decline in orders. Employment was consequently reduced even more sharply than in previous months. Signs of a de-escalation in the Iran conflict led to lower energy prices, which significantly reduced upward pressure on input and output prices. The build-up of stock levels to counteract supply bottlenecks eased, but the renewed lengthening of delivery times points to ongoing disruptions in supply chains”, said Bruckbauer, summarising the key survey findings.

Production expansion despite falling demand

Production expanded again in June, albeit at a slower pace than in the previous month. The production index fell to 50.6 points.

“The expansion in production was once again a consequence of building up stock levels to prepare for delivery failures and raw material shortages caused by supply chain disruptions resulting from the war in Iran. Although this led to some front-loading effects, new business fell significantly. Domestic orders fell more sharply than in the previous month, and export demand, which had still been rising in May, also weakened”, says UniCredit Bank Austria economist Walter Pudschedl.

The index for new orders fell to 48.5 points in June, the lowest level since January this year. At 48.9 points, the index for new orders from abroad was only marginally higher.

Job losses in domestic industry continued in June

As a result of weakening demand and high levels of uncertainty, staffing levels in Austrian industry were reduced at a faster pace than in the previous month. The employment index fell to 45.6 points, signalling the sharpest job losses in four months. Unemployment thus continued the slight upward trend seen in recent months.

The number of jobseekers in the manufacturing sector rose to almost 29,000 in June, corresponding to a seasonally adjusted unemployment rate of 4.4 per cent. Although the unemployment rate in the sector was low compared with the economy as a whole, which had an unemployment rate of 7.6 per cent, it was 1.4 percentage points – or 45 per cent – higher than the lows recorded at the start of 2023.

“In the coming months, given the challenging economic conditions, the slight upward trend in the unemployment rate is likely to continue. We expect the unemployment rate in manufacturing to rise to 4.5 per cent on an annual average in 2026, up from 4.3 per cent in 2025”, says Pudschedl.

The significant reduction in the workforce, despite a slight rise in production, suggests a further improvement in labour productivity in Austrian industry. This trend has now been ongoing for almost two and a half years, following massive losses in the wake of the COVID-19 pandemic.

Further build-up of stocks of purchases, but falling levels in stocks of finished goods

Although delivery times in the domestic industry lengthened significantly again in June, the increase was not quite as sharp as in the previous two months. Nevertheless, domestic firms increased their purchasing volumes for the fourth consecutive month since the outbreak of the war in the Middle East – and at a slightly faster pace than in May – in order to guard against supply disruptions and rising prices. In warehouse management, the focus therefore remained less on cost discipline and more on securing supplies of raw materials and inputs to prevent interruptions to production or sales. Stocks of purchases rose for the third month in a row, though not as sharply in June as in recent months.

“Whilst stocks of input materials and raw materials were again built up slightly in June, stocks of finished goods fell for the first time in nine months. What usually points to a healthy economy with strong customer demand is, in the current situation – characterised by a decline in orders – to be understood as a consequence of the ongoing supply disruptions”, said Pudschedl.

Falling energy costs dampened price momentum

June provided the first signs of easing inflationary pressure. The fall in the price of crude oil by more than 15 per cent compared with the previous month dampened cost pressures, primarily via fuel prices. Nevertheless, input prices rose very sharply in June. At 77.7 points, the input price index remained well above the levels seen before the outbreak of the war in Iran.

“The rise in output prices slowed in June by roughly the same extent as that of input prices, but was once again significantly lower overall than the cost dynamics in domestic industry”, says Pudschedl, adding: “It appears that, due to weak demand, businesses are unable to pass on the full extent of the cost increases to customers, meaning that profitability is likely to have deteriorated slightly on average once again – a trend that has held true for all but two months over the past two years.”

Enquiries:

UniCredit Bank Austria Economics & Market Analysis Austria

Walter Pudschedl, Tel.: +43 (0) 5 05 05-41957;

Email: walter.pudschedl@unicreditgroup.at