UniCredit Bank Austria Business Indicator Middle East conflict slows growth, but recovery should continue

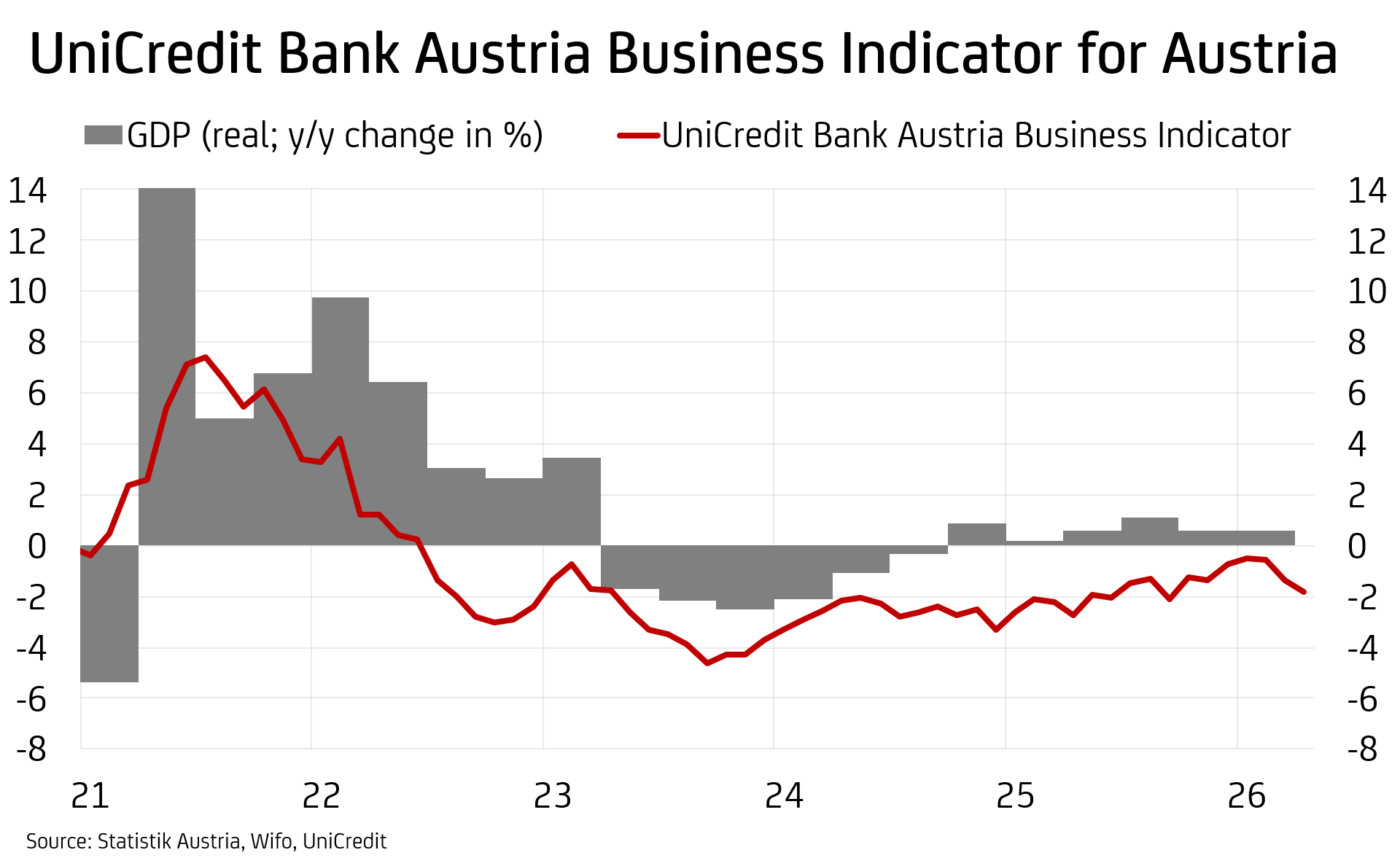

- A further deterioration in sentiment due to the ongoing Middle East conflict caused the UniCredit Bank Austria Business Indicator to fall to minus 1.8 points

- A sharp slump in consumer sentiment and sentiment in the services and construction sectors, though pessimism in industry eased slightly

- GDP forecast of 0.8 per cent for 2026 and 1.2 per cent for 2027, but rising risks of an economic slowdown as the Middle East conflict drags on

- Pressures on the labour market are mounting: the unemployment rate is expected to rise slightly to 7.5 per cent in 2026

- Inflation will not peak until towards the end of 2026

- A 25-basis-point interest rate hike in June is becoming increasingly likely

As the Middle East conflict drags on, economic sentiment in Austria has deteriorated further. The UniCredit Bank Austria Business Indicator fell to minus 1.8 points in April, its lowest level in six months,” says UniCredit Bank Austria Chief Economist Stefan Bruckbauer, adding: “Following the slight rise in GDP at the start of the year, we expect the domestic economy to continue on its path to recovery. However, the deterioration in sentiment at the start of the second quarter points to very subdued growth prospects, at least for the coming months.”

The 0.5-point decline in the UniCredit Bank Austria Business Indicator compared with the previous month was primarily due to the deterioration in sentiment among Austrian consumers. In view of geopolitical uncertainties and accelerating inflation resulting from already higher fuel prices and the resulting threat of a loss of purchasing power, consumer confidence was at its lowest level in two and a half years. Concerns about job security and fears of a deterioration in personal financial circumstances have increased, which could lead to greater caution in spending. As a result, service providers have already revised their business outlooks downwards.

Lower demand forecasts and the generally increased challenges posed by the changed operating environment weighed particularly heavily on sentiment in April within the transport and warehousing sector, as well as in the hospitality and accommodation sector and among travel agencies. Sentiment in the construction sector also deteriorated, partly due to rising costs, though this was attributable exclusively to the building construction sector. In civil engineering, as in domestic industry, business sentiment rose slightly, however, against a backdrop of stable demand. This was supported by an improvement in the export environment driven by somewhat more favourable global industrial sentiment emanating from the growth markets in Asia.

“Whilst sentiment in industry has eased slightly despite the continuing smouldering conflict in the Middle East, the outlook in the construction and services sectors deteriorated in April, particularly as consumer confidence fell significantly once again. Sentiment across all sectors of the domestic economy was in the pessimistic range at the start of the second quarter of 2026 – even further below the long-term average than in the previous month. Furthermore, sentiment in all economic sectors in Austria was worse than in the eurozone. The gap was once again particularly pronounced in industry, though it has been on a downward trend for the past two months,” says Bruckbauer.

Consequences of the Middle East conflict will certainly be felt well into winter

As the Middle East conflict drags on, the challenges for the Austrian economy are growing, and the consequences will certainly remain felt well into the winter. Even after the blockade of the Strait of Hormuz ends – which is unlikely to happen before the summer – supply chains will only return to normal after several months. Raw material prices will only gradually ease. However, by the end of 2026, prices will still exceed pre-conflict levels, particularly as ongoing uncertainty means that generally higher freight costs are to be expected, possibly further increased by a transit fee to Iran.

“Despite the already noticeable impact of the Middle East conflict on the Austrian economy, we expect the recovery to continue, although the pace will remain limited, particularly over the summer. We forecast GDP growth of 0.8 per cent for 2026, only slightly higher than in the previous year. Rising inflation will primarily weigh on consumption and push back the expected easing in the labour market until next year. It is not until 2027 that an acceleration in economic growth to 1.2 per cent, accompanied by a falling unemployment rate and lower inflation, is in sight,” says UniCredit Bank Austria economist Walter Pudschedl.

Easing on the labour market has stalleda

The economic recovery that had begun led to a stabilisation of the labour market situation from the second half of 2025 onwards. The annual average unemployment rate for 2025 stood at 7.4 per cent. However, signs of an easing have evaporated, at the latest with the onset of the Middle East conflict. In April, the seasonally adjusted unemployment rate rose to 7.6 per cent, the highest level in over four years.

Given the high level of uncertainty, the slow pace of recovery is not sufficient for a turnaround for the time being; however, the slower growth in the labour supply should at least keep the situation stable in the coming months. A gradual strengthening of economic momentum as a result of a step-by-step normalisation of supply chains and energy prices suggests an improvement in the unemployment rate, at least towards the end of the year.

“Following the rise in the unemployment rate from 7.0 to an average of 7.4 per cent in 2025, we now expect the upward trend to continue in 2026. However, despite the economic pressures caused by the Middle East conflict, the rise should slow significantly. We expect the unemployment rate to rise to 7.5 per cent in 2026, though with an improving trend already beginning to emerge over the course of the year. Supported by demographic factors, the unemployment rate should fall again in 2027 for the first time in five years, to an annual average of 7.4 per cent,” Pudschedl expects.

Inflation is set to rise even further in the coming months

After starting the year at low levels, inflation rose significantly in March and April to just over three per cent year-on-year, driven by rising fuel prices resulting from higher crude oil costs. Upward pressure on prices is set to remain strong in the coming months, despite the extension of the fuel price cap and the reduction in VAT on basic foodstuffs from 1 July. Oil and gas prices are merely leading a broader rise in commodity prices. Reduced transport capacity and rising insurance costs, as well as a general shortage of supply with low stock levels but high demand in the wake of the energy transition, have led to price increases for a whole range of industrial metals, such as copper. High energy costs are having a particularly strong impact on the production of aluminium and nickel, and production costs for chemical raw materials, as well as for fertilisers and batteries, have also risen. It is only in the coming months that these costs will be gradually passed on to selling prices and ultimately reflected in inflation.

“Inflation resulting from the Middle East conflict is not expected to peak until towards the end of 2026, with figures exceeding 3.5 per cent. Thanks to low inflation at the start of the year, we expect an annual average inflation rate of 3 per cent for 2026. For 2027, we anticipate only a moderate slowdown in inflation to an average of 2.6 per cent due to expected second-round effects,” said Pudschedl.

ECB interest rate hikes expected

“We expect the ECB to raise interest rates by a total of 50 basis points in June and September, although we are now very confident about the June hike. From the ECB’s perspective, moderate interest rate hikes would anchor inflation expectations and prevent significant second-round effects, whilst limiting damage to the economy and employment. However, in our view, the risks are asymmetrically distributed. Given the development of the geopolitical situation, the probability of a scenario involving stronger measures by the ECB is significantly higher than that of a cautious scenario,” concludes Bruckbauer.

Enquiries:

UniCredit Bank Austria Economics & Market Analysis Austria

Walter Pudschedl, Tel.: +43 (0) 5 05 05-41957;

Email: walter.pudschedl@unicreditgroup.at